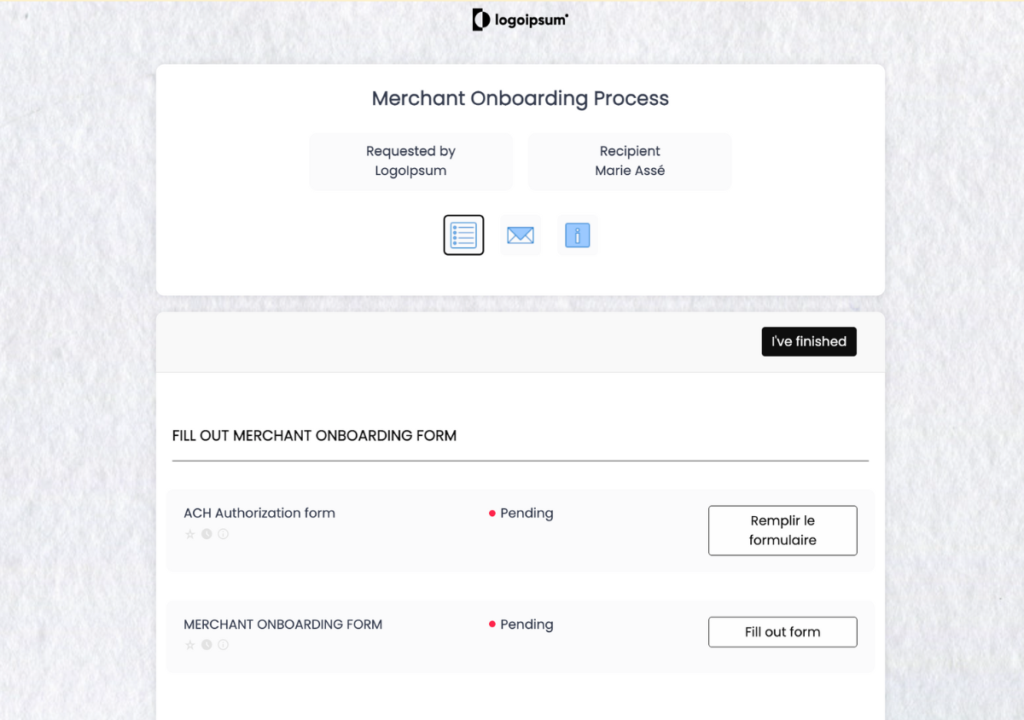

A digital onboarding process template used by payment service providers to review, approve, and activate merchants.

A merchant onboarding process defines how payment service providers (also called PSPs) collect, verify, review, and approve merchants before enabling them to start accepting customer payments.

This process cannot be completed effectively using single form builder or legacy tools. It requires a robust end-to-end process that brings together business verification, identity verification, compliance checks, risk assessment, and operational validation into a repeatable workflow to ensure seamless payment processing.

For PSPs, acquiring banks (merchant acquirers), and other financial institutions, merchant onboarding sits at the intersection of secure payment processing, regulatory obligations, and risk management processes.

The quality of the merchant onboarding journey directly impacts how quickly merchants can be onboarded, how reliably new merchant accounts are approved, and how effectively risks related to money laundering, terrorist financing, fraud risk, or delayed or failed transactions are controlled.

Clustdoc provides you with a ready-to-use merchant onboarding process template that will ensure that each merchant is assessed consistently, that required data is collected once and reused across teams, and that decisions are documented throughout the onboarding lifecycle.

Clustdoc merchant onboarding process template is designed to support organizations that onboard merchants at scale while operating in regulated payment environments.

It would typically be used by financial services such as:

• Payment service providers (PSPs) managing large volumes of merchant onboarding requests

• Acquiring banks (merchant acquirers) responsible for approving and maintaining merchant accounts

• Financial institutions involved in payment processing solutions and settlement

• Payment platforms enabling third‑party sellers or merchants to start accepting payments

The template breaks down the process into single steps that aligns commercial onboarding with compliance and risk requirements. The goal here is automate how PSPs coordinate data collection, document collection, compliance reviews, and approvals without relying on emails, spreadsheets, or disconnected systems anymore.

Our merchant onboarding process template follows a series of well organized steps. Each step supports both operational efficiency and regulatory control. Once you’ve downloaded this template, you can adjust it to match your business requirements very easily from the Clustdoc admin console.

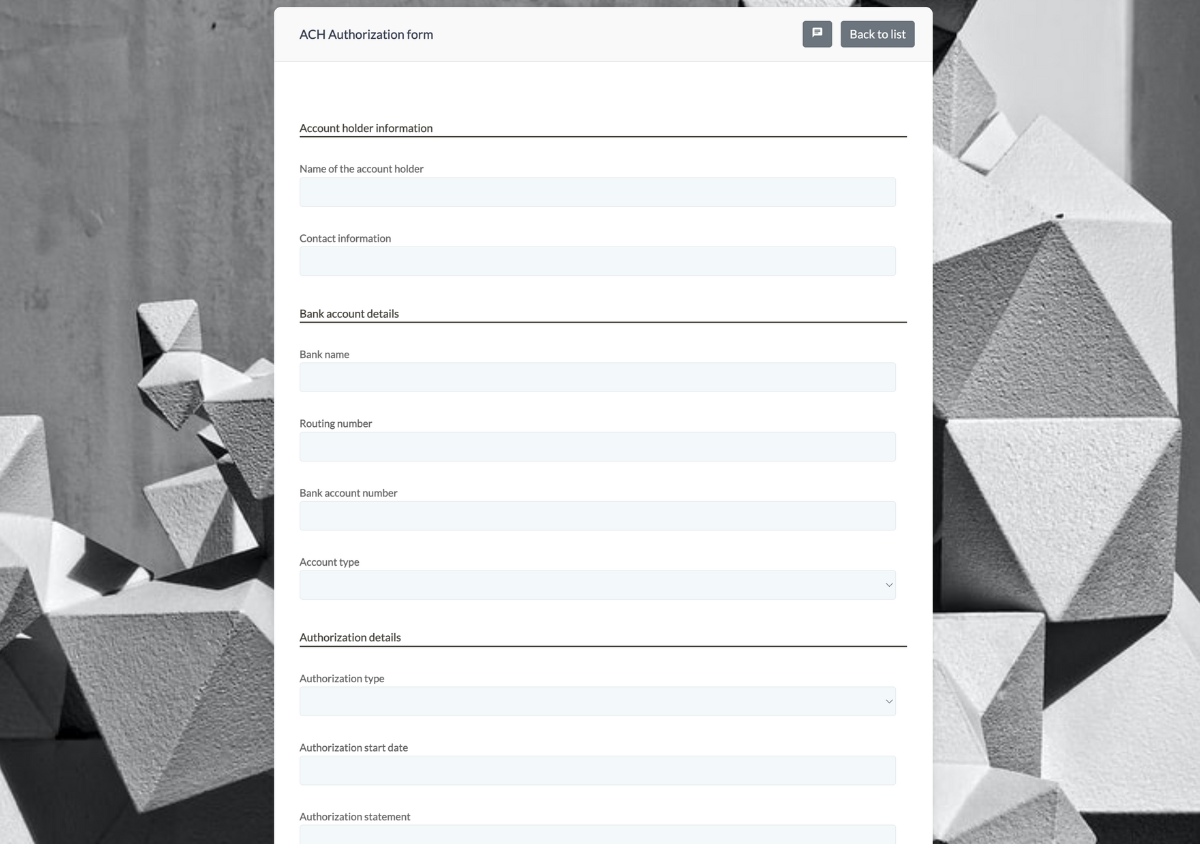

Our process template starts with collecting core merchant information through a merchant onboarding form. This stage establishes the merchant’s identity and legal existence before any payment processing activity begins.

Typical data collected at this stage includes:

• Legal business name and trading name

• Registered address and operating address

• Business registration documents

• Ownership structure and control information, including personal identification documents for beneficial owners

• Tax identification number and employer identification number

• Details required to create merchant accounts

• Business’s financial health information such as financial statements, income statements, cash flow statements, and previous transaction volumes

• Detailed business plan and revenue projections

Based on the above information, the rest of the onboarding workflow will be dynamic, ensuring that all relevant documents and business information are captured in a standardized way.

Once basic merchant data is collected, PSPs must perform compliance checks aligned with KYC (Know Your Customer) and AML (Anti Money Laundering) requirements.

These checks typically involve:

• Verifying the legitimacy of the business and its beneficial owners through identity verification and document verification

• Validating ownership structure and control relationships

• Screening against relevant sanctions, watchlists, and lists related to terrorist financing

• Assessing exposure to money laundering risks and fraud detection

KYC and AML controls are critical for financial institutions involved in merchant onboarding.

So, embedding these checks directly into your onboarding process reduces rework and helps ensure that no merchant proceeds to payment processing without proper validation

Risk assessment is a central component of any merchant onboarding process. At this stage, payment service providers evaluate the merchant’s risk profile based on multiple factors.

This assessment often considers:

• Merchant’s business model and transaction types

• Industry classification, including identification of high risk industries

• Geographic exposure

• Expected transaction volumes and payment behavior, including transaction limits

Using this template, you can define scoring rules to determine what level of risk is associated with each merchant record created through the Clustdoc merchant portal.

This really helps PSPs and acquiring banks teams streamline risk management by automatically applying proportionate reviews rather than treating all merchants the same way.

After risk classification, the template includes internal due diligence tasks that will allow financial and operational checks to be performed in order to confirm that the merchant can operate sustainably within the payment ecosystem.

This stage may include:

• Review of financial statements, income statements, and cash flow statements

• Analysis of prior payment processing history, where available

• Assessment of revenue flows and settlement expectations to ensure sufficient funds

These due diligence tasks can help your teams understand how merchants will use payment processing services and whether their activity aligns with stated business operations.

Once compliance, risk assessment, and due diligence steps are completed, your Clustdoc onboarding process moves to approval and activation.

This phase typically involves:

• Review and approval by the acquiring bank (merchant acquirers)

• Creation and configuration of merchant accounts and new merchant account setup

• Connection to payment gateways and payment processing platform integration

• Final validation before accepting payments to ensure secure payment processing

Merchant onboarding does not conclude once a merchant account is activated. Ongoing activities such as renewals, periodic Know Your Customer (KYC) or Know Your Business (KYB) checks, and recurring compliance reviews are essential to maintain regulatory adherence and effectively manage risk over time.

These recurring checks typically include regular updates and verification of merchant data and ownership structures as well as scheduled KYC/KYB renewals to confirm the legitimacy of merchants and their beneficial owners.

And on top of the above, continuous transaction monitoring aligned with updated risk profiles, reassessments for merchants operating in high-risk industries or with changing business models, and persistent controls to prevent money laundering, detect fraud, and ensure compliance with evolving regulations must also be performed after the onboarding process.

If your merchant onboarding process relies on disconnected forms, manual reviews, or ad-hoc coordination between teams, it becomes difficult to scale while maintaining control.

Using a dedicated merchant onboarding process in Clustdoc allows you to centralize data collection, compliance checks, risk assessment, and approvals in a single workflow. You can standardize how merchants are onboarded, adapt reviews based on risk profiles, and maintain full visibility from initial application through ongoing monitoring.

Create your account to start configuring your merchant onboarding process and see how Clustdoc supports payment service providers and financial institutions in managing merchant onboarding at scale.

The merchant onboarding process generally requires several key documents and details, including business registration papers, ownership structure information, KYC documentation, tax identification numbers, and financial records. These elements are essential to evaluate risk and facilitate the creation of merchant accounts.

Yes. The process can be configured to reflect your existing KYC, anti money laundering, and risk assessment policies. You can adjust required data, review steps, and approval paths without redesigning the entire workflow.

Clustdoc allows compliance, risk, and operations teams to collaborate within the same process. Each team reviews the information relevant to them, adds comments or decisions, and moves the merchant forward without duplicating work.

No. Business and compliance teams can update steps, forms, and requirements directly as policies or regulations evolve, without relying on technical development.ncial institutions to manage changing risks related to merchant behavior, transaction patterns, and potential money laundering activities.

Try Clustdoc today, launch your new workflow tomorrow.