Opening a merchant account is a structured and often rigorous process.

Merchant account providers and acquiring banks must review a merchant’s legal information, evaluate the business model, confirm financial stability, and determine whether the company can securely process credit card transactions or handle customer payments at scale.

A clear merchant application checklist helps both new businesses and established companies gather the required documents and avoid delays during the underwriting process.

We’ve designed this merchant application checklist template for Clustdoc to help you centralize every step of your merchant onboarding workflow.

Instead of chasing documents through email chains or juggling between tools, you can collect everything in one secure, digital process.

This article outlines the key information providers typically need, the documents that support verification, and how our template structures the entire application process to reduce friction for both your underwriting team and your merchants.

Merchant accounts expose providers to financial liability.

To mitigate these risks, merchant account providers require a consistent application process supported by documents that verify legal identity, financial stability, and business operations.

That’s exactly why we built this merchant application checklist.

It ensures that the company’s full legal name, business address, and ownership details are captured accurately from the start.

Your team can verify taxpayer information like EIN, taxpayer identification number, or run KYC checks on key individuals without hunting through emails.

Financial statements, bank statements, and other required documents flow directly into your underwriting pipeline, giving your team everything they need for the initial risk assessment in one organized place.

Companies that provide credit card payments or act as a payment gateway rely heavily on complete, accurate information to determine whether the merchant qualifies for lower fees, standard pricing, or higher fees due to risk factors.

With Clustdoc, you get that information upfront, structured consistently across every application.

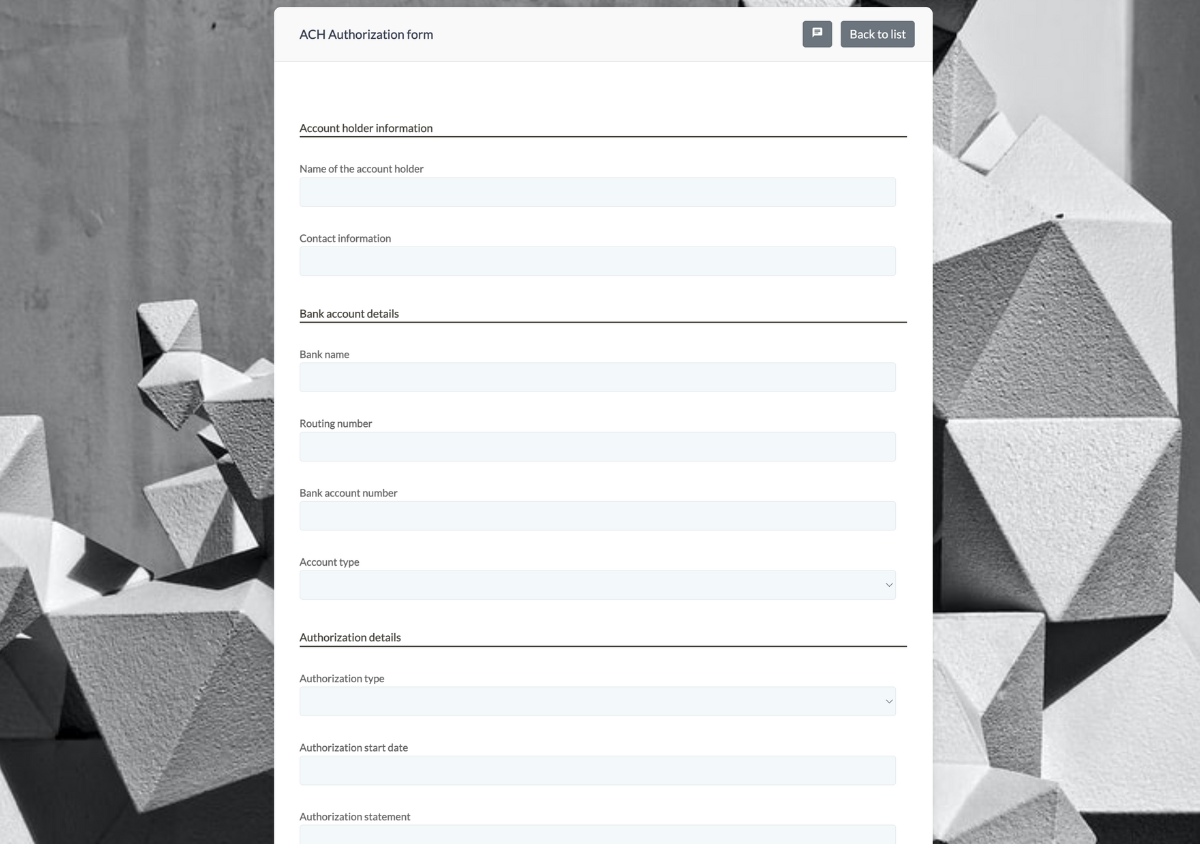

Business information and legal documentation

Our template guides merchants through submitting their legal name, full legal name of business owners, corporate structure (corporation, LLC, partnership, or sole proprietorship), business license, and business address or physical address.

Merchants provide their mailing address, website, description of business processes, and any additional documentation that validates their operations. Everything gets organized automatically in your Clustdoc workspace.

Taxpayer and identification details

To help you comply with regulatory and banking requirements, the workflow collects employer identification numbers (EIN) or taxpayer identification numbers.

Financial statements and supporting documents

Your underwriting team can review financial statements, bank statements, historical revenue, and other indicators of financial stability directly in the workflow.

New businesses can upload business plans, projected transaction volumes, or any documentation showing their ability to support future payments.

And everything stays organized in one place.

Details of products, services, and business model

Our checklist helps you evaluate the merchant’s business model, products sold, service delivery processes, refund policies, and operational workflows. You can see how the company interacts with customers, manages customer payments, and handles potential disputes or chargebacks, all documented in a structured format.

Transaction and payment details

Merchants provide expected monthly transactions, average ticket size, and maximum transaction amounts through guided fields.

These details influence the merchant’s risk profile and your underwriting decision, and they’re captured consistently every time.

A complete merchant account application checklist in Clustdoc prevents repeated document requests, reduces incomplete submissions, and accelerates underwriting.

For your team, it ensures that core verification data like legal identity, business information, bank account details, and financial stability is collected the same way across all merchants.

For businesses applying, it clarifies exactly what’s expected, reduces frustrating back-and-forth, and supports faster approval with better processing terms.

Plus, with Clustdoc’s workflow automation, you can set up smart reminders for missing documents, route applications to different reviewers based on risk factors, and maintain a complete audit trail of every merchant interaction.

We’ve built this template specifically to streamline merchant onboarding inside Clustdoc.

Import it into your workspace and start collecting all required documentation upfront, maintaining consistent underwriting standards across every application, and giving merchants a clear, professional experience from start to finish.

You can customize every field to match your specific requirements, automate follow-ups, and keep your entire merchant pipeline organized in one secure platform.

Yes. Inside the application form of this checklist, questions related to products, refund policies, delivery times, financial stability, and transaction projections highlight early warning signs.

You can create compliance workflows based on merchants answers to route the application to the right reviewers.

Your compliance team can then identify high-risk patterns, such as high average ticket size, negative cash flow, or service-delivery delays, before onboarding is completed.

Yes. Teams spend less time chasing documents, validating IDs, or interpreting unclear business models. This reduces operational load, improves throughput, and frees compliance and underwriting teams to focus on high-risk or complex merchants rather than managing avoidable bottlenecks.

Try Clustdoc today, launch your new workflow tomorrow.