✪ Your digital process automation expert

A reliable Know Your Customer KYC checklist is the key to making your onboarding process run like clockwork, especially when you’re dealing with a multitude of customer types, different products, and fast turnaround expectations.

A KYC checklist is an operational bridge between policy and execution: it standardises customer identification, makes sure you’ve done your due diligence, help support a risk-based approach, and demonstrate compliance to auditors or internal stakeholders when they ask you to ‘show me what happened and why you approved this business relationship‘.

At Clustdoc, we’re seeing teams use a KYC checklist process for one simple reason: to ensure they’re staying on top of compliance against internal controls and regulatory requirements.

But we’re also hearing that they’re doing it because they want to reduce friction for legitimate customers without letting their guard down and skipping identity verification or ongoing monitoring for high-risk transactions.

When your process is done right, the same KYC checklist that reduces money laundering and terrorist financing risk can also improve the customer experience, customer trust, and therefore, overall customer satisfaction.

A KYC checklist is a structured customer checklist your team uses to get through the Know Your Customer steps before (and during) a business relationship.

It captures the customer information and evidence you need, how you’ve verified it (eg. verifying the customer’s identity), how you’ve documented customer risk, and how you stay on top of ongoing compliance through continuous monitoring and periodic reviews.

In a mature KYC program, the checklist really is your control tool that ties your KYC procedures, customer identification program, and customer due diligence approach together.

For financial institutions and many financial service providers, that is essential to align with a broader regulatory framework (but also local regulations and internal compliance requirements) which expects consistent onboarding controls, clear escalation paths for high-risk cases, along with a solid record keeping.

You’ll hear teams refer to this as a Know Your Customer checklist or ‘the KYC steps.’

In any case, you should have at least a documented and comprehensive KYC checklist that your team can run the same way every time.

Most teams usually need to use a KYC checklist at three points in the customer lifecycle:

This is the most obvious use: the KYC checklist makes sure customer identification, baseline customer due diligence, and an initial risk assessment get done before the account is activated or services start.

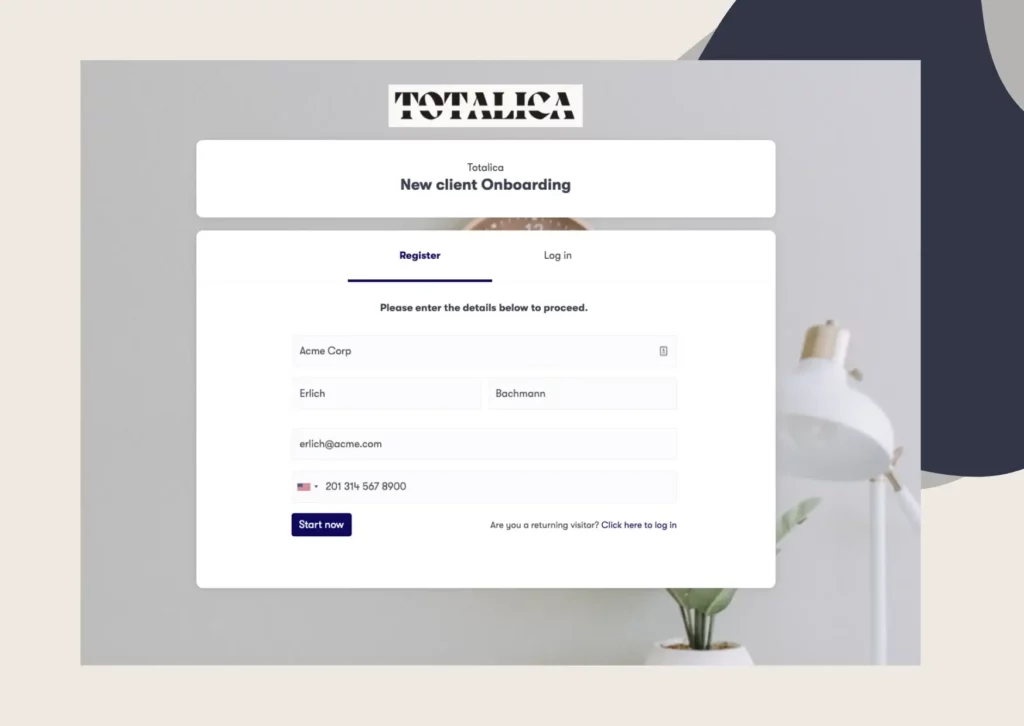

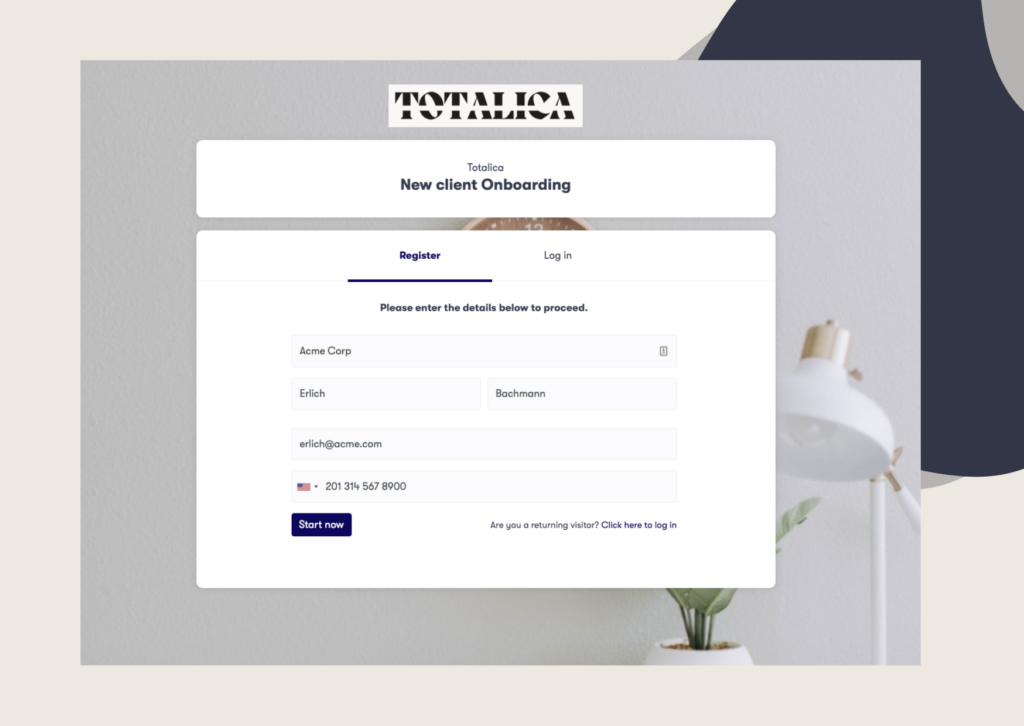

A checklist like this is much easier to manage when it lives inside a structured onboarding workflow.

In Clustdoc, your teams can turn their KYC checklist into a guided client portal where required documents, identity verification steps, and due diligence questions and steps are completed in one organized workflow before the account is approved.

If a customer’s profile changes (new ownership, new control, new geography, new product usage), the KYC compliance process typically means updating customer information, reassessing customer risk profiles, and refreshing KYC documents, this could also be an ongoing process.

Because customer profiles can change over time, many organizations maintain internal records to track updates.

With Clustdoc, teams can run KYC renewals campaigns to request refreshed documents and capture new information while keeping the entire KYC history organized.

In this case, your KYC checklist becomes part of ongoing monitoring or continuous monitoring, including transaction monitoring, reviewing customer behaviour, and periodic reviews based on risk tiers.

For example, you may need to run new KYC checks on your current base of customers every year.

For high-risk customers, the cadence is typically tighter and the documentation expectations are higher.

KYC checklists gather a set of operational tasks and controls that must happen to ensure compliance.

Your team should be able to answer:

• what did we collect,

• what did we verify,

• what risks did we assess,

• what exceptions did we approve?

This clarity is essential for maintaining a transparent and auditable KYC process.

Many teams structure the first part of their KYC checklist around a customer identification program, often referred to as a customer identification program CIP.

Concretely, this means that you’d clearly define the required customer identification data points and acceptable evidence for identity verification.

For example, a bank’s KYC checklist might include collecting a customer’s government-issued identification, such as a passport or driver’s license, along with proof of address like a recent utility bill or bank statement.

Then, the bank’s compliance team would verify the authenticity of the ID and ensure it matches the customer’s provided information, confirming the customer’s identity before opening an account.

For individuals, you’d at least need to collect:

• a government-issued ID,

• date of birth,

• address, and, where applicable,

• a tax identification number.

Additional documents such as utility bills or bank statements may be used to verify the customer’s address or source of funds, depending on the risk model and local regulations.

The goal is to establish solid customer identification that withstands scrutiny.

After identity is established, customer due diligence typically shifts from ‘who is the customer?‘ to ‘what is the risk of doing business with them?‘

This is where your due diligence gets more risk-based: you’d capture customer information about occupation or business activity, expected activity, geography, product intent, and any contextual risk indicators.

Ideally, you’d want to keep things separate:

baseline customer due diligence (often referenced as customer due diligence CDD) and enhanced due diligence for high-risk scenarios.

A short, documented risk assessment, with defined risk profiles and customer risk profiles, is what makes your decision explainable down the line.

A strong KYC compliance workflow includes screening steps (sanctions/PEP where relevant) and adverse media screening.

When the customer or a related party gets flagged, especially for politically exposed persons, you need a clear escalation path and a defined approval authority.

At this stage, it’s about documenting the review, linking the evidence, and recording how your team resolved potential indicators of financial crimes, financial fraud, money laundering, terrorism financing, or other financial crimes.

When you’re putting together your checklist, be sure to leave some room to note down which regulatory requirements or internal policies triggered a particular case (like when you need to bring in extra due diligence).

If you’re operating in the US, you might want to reference what the financial crimes enforcement network expects; globally, you’ll want to look at the financial action task force recommendations – but you need to check with your internal counsel or compliance team to figure out exactly how it all applies to your business.

We can help you run your KYC checklist as a flow that guides your team:

you can collect structured customer data through online forms, ask for the right KYC documents based on customer type and apply validation rules that reduce all the back-and-forth.

Next, you can route high risk cases to the right person, store all the evidence in one place and keep consistent records for the government or auditors when they come knocking.

Most importantly, Clustdoc helps you turn KYC updates into a real thing: you can schedule periodic reviews, trigger re-verification tasks and keep the KYC process tied to the business relationship automatically.

If you’re already using automated systems (screening, monitoring or decision support), we can structure the workflow around those tools and keep all the reviewer conclusions on record, supporting a much stronger compliance process from start to finish.

A good KYC checklist is a practical tool that supports your know-your-customer obligations while saving your team time and keeping your customers’ trust intact.

By putting together a clear customer identification process, consistent due diligence for customers, documented risk profiles and ongoing monitoring, you can build a KYC program that scales, especially if you’re a financial institution that’s under a lot of scrutiny and dealing with changing regulatory requirements.

Clustdoc helps compliance and operations teams run these KYC workflows through a secure client portal where documents, identity information, and due diligence steps come together in one organized client file.

If you’re looking for a more structured way to manage KYC onboarding and ongoing compliance, we’re here to help.

A well crafted KYC checklist will show your team has done the right compliance steps. It records how identity checks were done, how risks were assessed and who approved the final decision.

For regulators this matters since it shows your organisation has taken real measures against money laundering and other financial crimes.

When managed in Clustdoc the same checklist can store supporting documents, track reviewer activity and keep a timestamped record of every step, making regulatory reviews and internal audits much easier to manage.

When it comes to figuring out who someone is, use a mix of reliable docs and consistent review procedures.

Lots of companies start with a government id and proof of address.

These days, more and more teams are also using digital identity checks to automate ID validation and match it up with whatever documents come in.

A good diligence checklist will show what evidence you collected and how you confirmed the identity.

When you run this workflow in Clustdoc, you can request ID docs as part of your end-to-end onboarding process and run all appropriate checks at once.

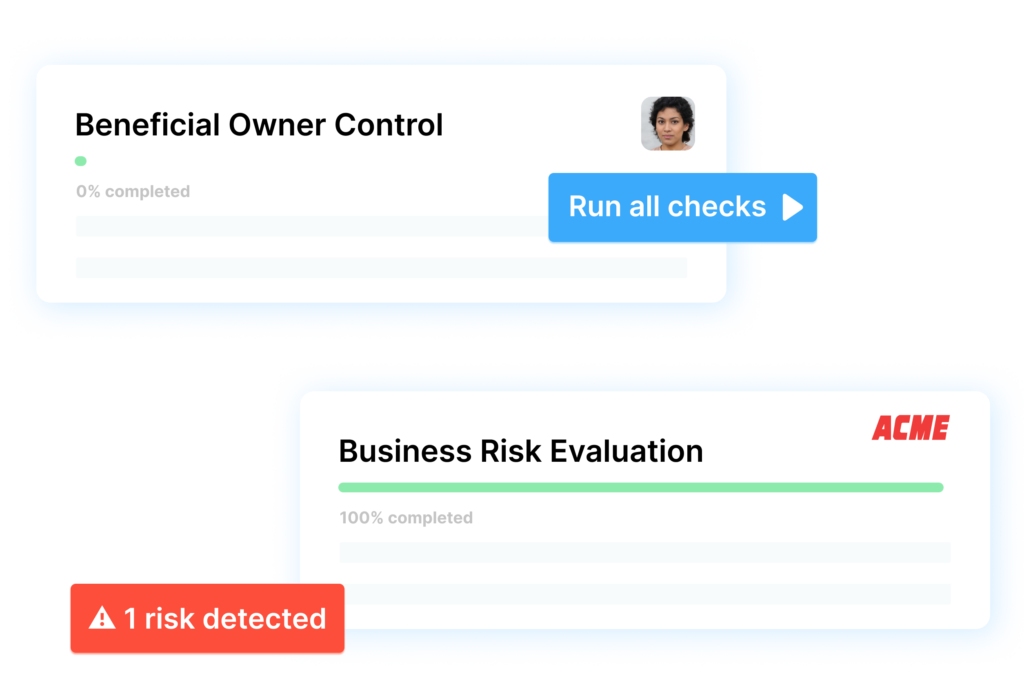

When onboarding a company you need to figure out who the power-players are (the beneficial owners) and verify their identities.

This is part of due diligence.

Your team needs to capture ownership info, confirm who’s in control and run an id verification on each beneficial owner where required.

This is where a background check and structured data collection really comes in handy.

A checklist should guide reviewers through who to check, what to look for and if the ownership structure adds any extra risk. Clustdoc makes it easy to collect ownership info and documents through guided forms, and if you prefer, you can also run these checks in the background automatically.

Share this with your team